The conventional view (the Greenspan put)

|

Stimulus policies increase moral hazard.

Anticipating to be rescued in downturns, firms might take more risk today.

|

Our contribution

|

Figure: Countries with new or existing wage subsidy schemes

during the Covid-19 pandemic (Sources: ILO, IMF, authors’ calculations)

Figure: Countries with new or existing wage subsidy schemes

during the Covid-19 pandemic (Sources: ILO, IMF, authors’ calculations)

|

Intuition behind our result

Absent intervention

Intuition behind our result

Introduction of the wage subsidy

Intuition behind our result

Firm's risk allocation response

Intuition behind our result

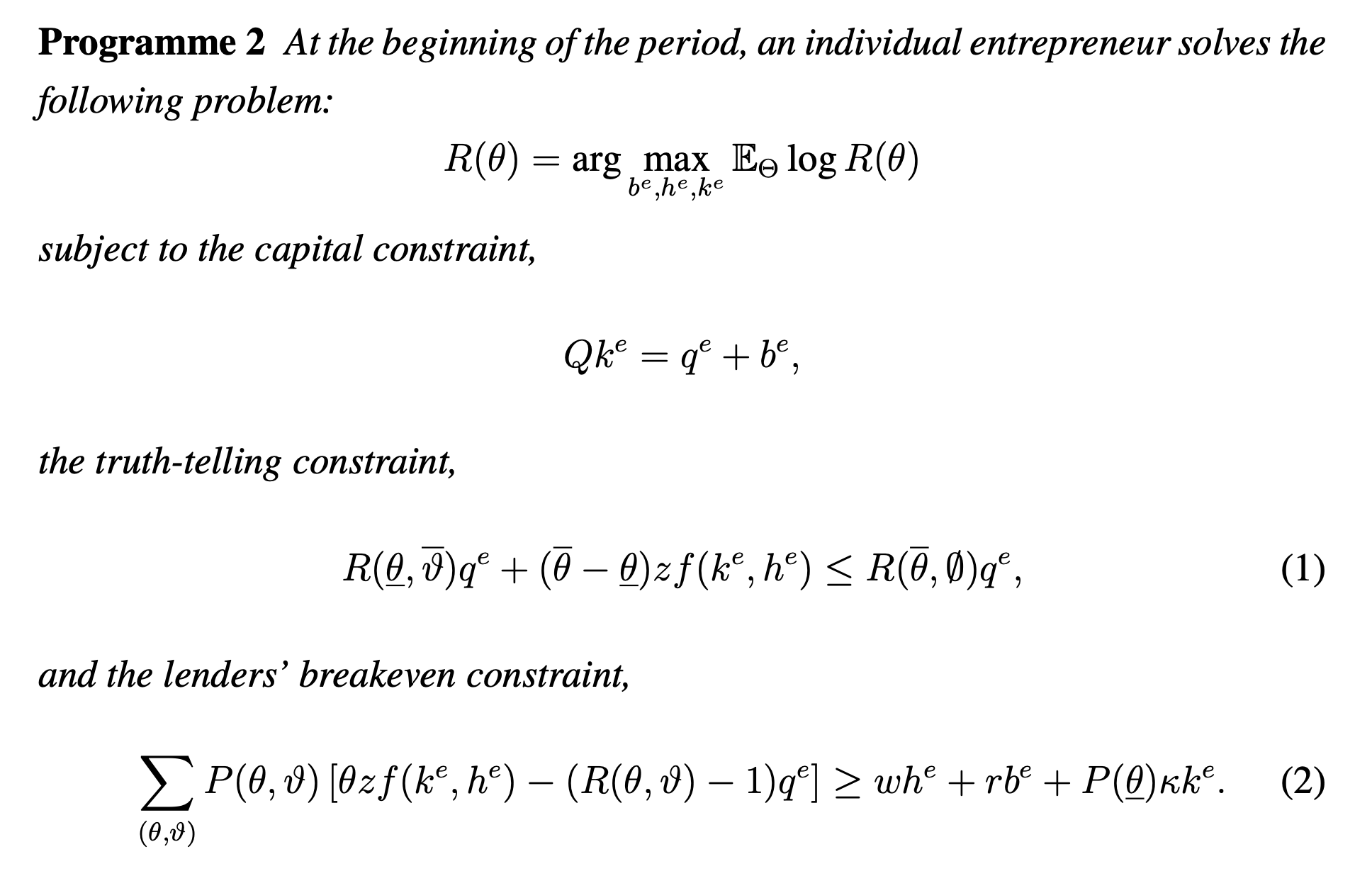

The entrepreneurcombines their own wealth with borrowed wealth and labour. Contracts are endogenously incomplete. Entrepreneurs can hide income from external creditors. External creditors can audit the firm and uncover hidden income, but these audits are noisy. (Duncan and Nolan, 2019) |

.jpg)

|

The entrepreneur's intratemporal problem

|

Extension |

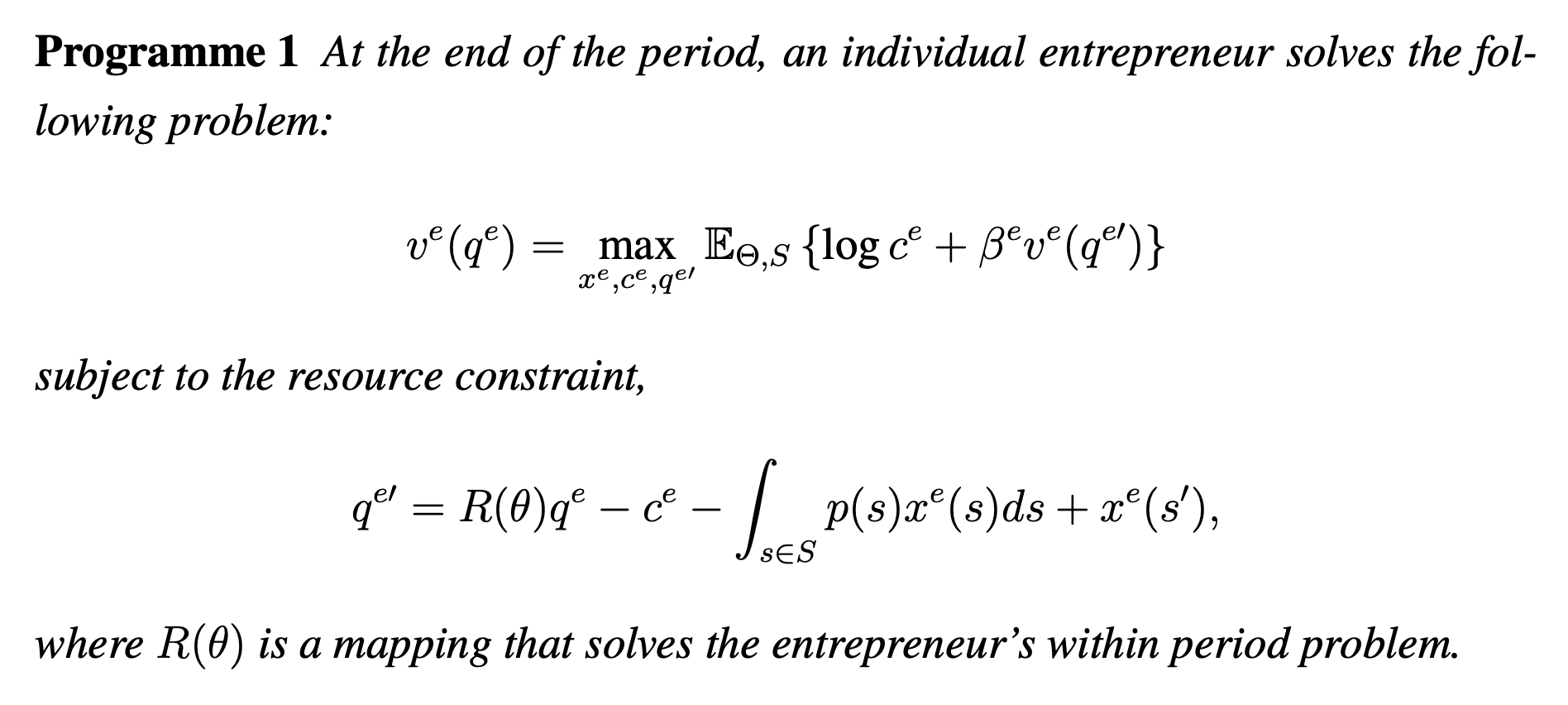

The entrepreneur's intertemporal problem

|

captures trade in aggregate state contingent securities. Markets for aggregate risks are complete. |

Expected welfare effects of wage subsidy simple rules

Welfare gain is expressed as a share of business cycle welfare losses.

Shaded area indicates 90% credible interval.

Persistence of TFP shocks

Welfare gain is expressed as a share of business cycle welfare losses.